Life has a way of throwing unexpected financial curveballs when you least expect them. Whether it’s a sudden mountain of accumulating medical bills, a steep rise in high-interest debt, or a major business downturn, it’s remarkably easy to find yourself in a position where your monthly income can no longer keep pace with your financial obligations. When bills pile up, the emotional and financial strain can quickly become suffocating, casting a shadow over your daily peace of mind.

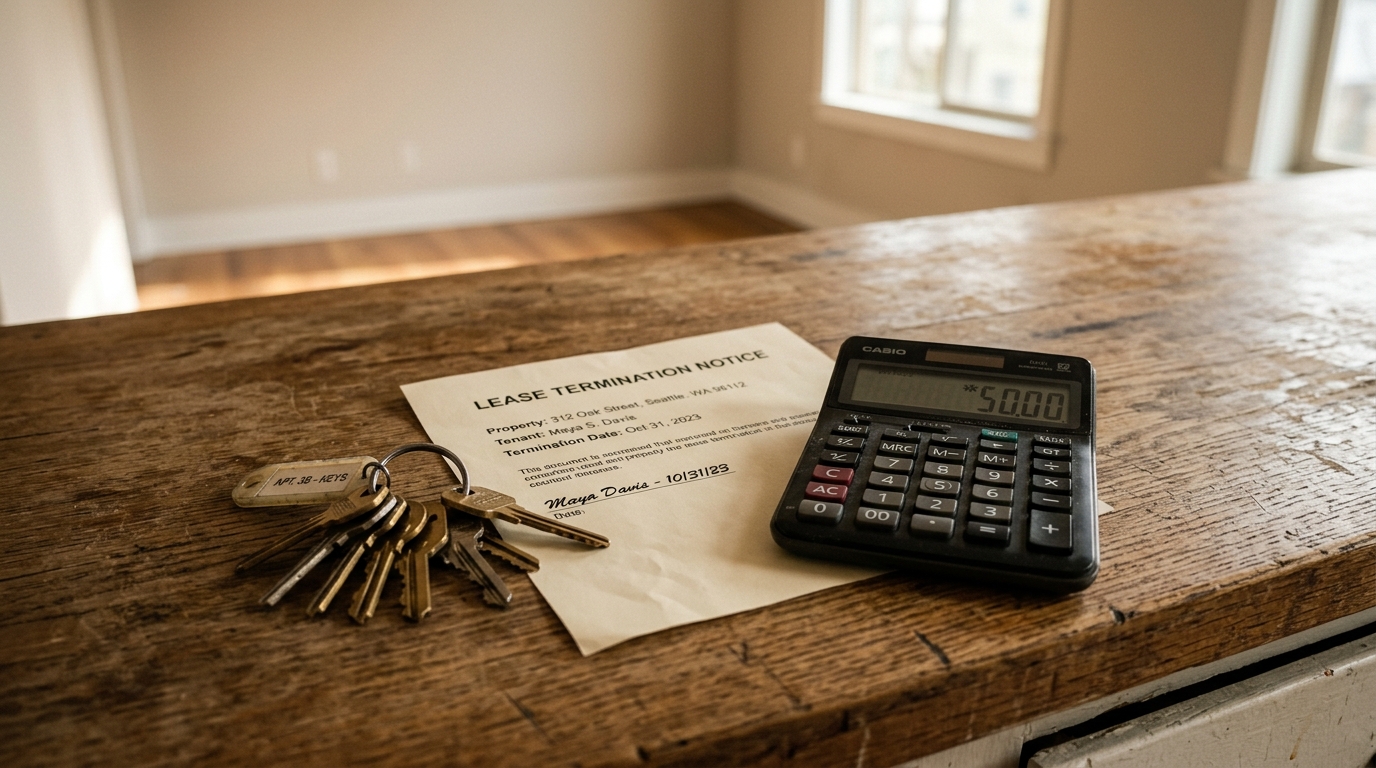

For property owners navigating an urgent cash crunch in North Texas or Southwest Oklahoma, real estate represents both your largest asset and your greatest potential lifeline. Your home likely holds thousands of dollars in built-up equity—wealth that could completely wipe out your debt and give you a clean slate.

However, when you need cash to stabilize your life right now, the traditional real estate market is an incredibly flawed vehicle. Trying to list a property through conventional retail channels while trying to pay off pressing debts is a slow, stressful race against time. Let’s pull back the curtain on the realities of listing a home under financial pressure and explore why selling directly to a local cash home buyer is often the fastest, safest, and most effective way to unlock your equity and regain total financial control.

The Relocation Trap: Why the Traditional MLS Fails an Urgent Financial Need

Hiring a real estate agent to place your property on the Multiple Listing Service (MLS) is a process built entirely for sellers who have the luxury of time. When you are liquidating an asset to resolve outstanding bills, a conventional retail sale exposes you to several major roadblocks:

1. The Sluggish Traditional Timeline

A conventional real estate transaction is notorious for its slow, multi-stage schedule. From finding a qualified retail buyer and waiting on home inspections to navigating the labyrinth of bank underwriting, a standard retail sale typically takes 60 to 90 days just to reach the closing table. If you have utility companies, medical collectors, or credit card issuers demanding payment within weeks, a multi-month traditional real estate delay simply doesn’t help you.

2. The Bleeding of Equity via Ongoing Holding Costs

Every single month your house sits on the market is another month you must personally fund its operational expenses. You are still legally responsible for paying the mortgage, property taxes, structural insurance, and monthly utility bills on a home you are actively trying to exit. If you are already struggling to pay your regular bills, maintaining the holding costs on a retail listing will only deepen your financial hole and drain the equity you are trying to rescue.

3. The Out-of-Pocket Repair Catch-22

Retail buyers expect move-in-ready properties and utilize strict home inspection contingencies to protect themselves. If a buyer’s inspector flags an aging roof or a system deficiency, the buyer will demand that you fix it before closing. This creates a brutal financial catch-22 for a homeowner under a cash crunch: you are forced to spend thousands of dollars in liquid cash that you don’t have on property repairs just to keep a fragile retail deal from falling apart.

Real-World Case Studies: Listing vs. A Direct Cash Sale

To see how a direct cash sale can mean the difference between financial recovery and long-term credit damage, let’s examine two contrasting real-world scenarios.

Case Study A: The Conventional Listing Debt Spiral (The DFW Metroplex)

A homeowner in the Dallas/Fort Worth area accumulated substantial medical debt following an unexpected illness. Desperate to liquidate the home’s equity to pay off the collection agencies and protect their credit score, they listed the home at full market value with a traditional real estate agent.

- Month 1–2: The home hits the MLS. The owner spends precious cash formatting the home for staging and keeping the utilities running for open houses. A retail buyer finally makes a strong offer, and a contract is signed.

- Month 3: The buyer’s home inspector discovers a plumbing leak behind the bathroom wall. The buyer’s mortgage lender refuses to fund the loan until a licensed contractor repairs the utility line and clears the mold. The seller does not have the liquid cash to fix it, and the deal collapses.

- Month 5: Having now fallen behind on both the medical bills and their monthly mortgage payments due to ongoing holding costs, the homeowner’s credit score drops significantly. The bank issues a formal notice of default.

- Month 7: The owner is forced to accept a deeply discounted investor offer just days before a scheduled foreclosure auction, walking away with virtually zero net proceeds after paying the agent’s 6% commission.

Case Study B: The Swift Cash Resolution (Lawton, Oklahoma)

A property owner in Lawton, Oklahoma, faced a sudden business downturn that left them with mounting high-interest credit card debt and back taxes. Recognizing immediately that their equity was the cleanest way to wipe the slate clean, they decided to liquidate their property asset immediately to create a financial safety net. They bypassed the traditional retail market entirely.

- Day 1: The homeowner contacts an established direct cash home buyer via a simple online form.

- Day 2: A local property coordinator reviews the neighborhood data and schedules a single, quick, non-invasive walkthrough to assess the property’s layout.

- Day 3: The company extends a firm, transparent all-cash offer. The valuation is clear, featuring no hidden corporate fees, service deductions, or mandatory repair items.

- Day 5: The owner accepts the offer and selects a guaranteed closing date just 10 days away. No bank underwriting guidelines or mortgage appraisals are required.

- Day 15: The transaction closes smoothly at a trusted local title company. The cash buyer pays off the existing mortgage balance completely, and the remaining equity is wired directly into the homeowner’s bank account. The seller uses the immediate cash to settle their debts in full, protecting their credit score and regaining complete peace of mind.

Why a Direct Cash Buyer is Your Best Financial Recovery Tool

When you sell your property directly to an established investment company like ours, you eliminate the uncertainty, delays, and out-of-pocket expenses of the traditional retail market. We specialize in providing the speed and certainty that urgent financial shifts require:

We Can Close in Days, Not Months

Because we utilize our own private liquid capital, we completely cut out the weeks of waiting required by bank underwriters, mortgage processors, and appraisal disputes. We can close transactions in as little as 7 to 10 days, allowing you to halt your monthly housing expenses immediately and extract your cash equity before you fall behind on payments.

We Buy 100% As-Is (Keep Your Capital in the Bank)

You do not need to spend a single dime on paint, landscaping, cleaning, or structural updates. We buy houses completely as-is. If the home requires maintenance or cosmetic modernizations, our team takes on 100% of the construction risk and expenses internally after closing, allowing you to keep your vital cash reserves exactly where they belong.

Zero Commissions or Hidden Closing Costs

Traditional real estate sales force you to hand over roughly 6% of your home’s final sale price to agent commissions, plus another 2% to 3% in title fees and buyer closing costs. When you are facing a cash crunch, losing 8% to 10% of your equity to transaction fees cuts deep. We charge zero commissions and cover all standard closing costs, ensuring that every single dollar of our offer goes directly into your pocket.

Unlock Your Equity and Take Control of Your Timeline

Accumulating bills should not hold your financial future hostage or compromise your long-term credit profile. You do not have to let an unpredictable, slow-moving retail market or expensive repair demands dictate your recovery timeline.

If you are ready to secure an immediate, guaranteed sale, eliminate the stress of ongoing holding costs, and walk away with a substantial financial safety net on a timeline that you completely control, a direct cash sale is your cleanest path forward.

To see exactly how our direct home-buying model cuts through the red tape of the traditional market, take a moment to look over our transparent guide explaining how the direct cash-buying process works. We believe in providing straightforward operational facts so you can make an informed, confident decision for your financial security.

For property owners navigating an urgent cash crunch or debt consolidation in North Texas, you can reach our localized underwriting team directly by visiting our trusted real estate investors page for the DFW area to request a rapid, no-obligation cash evaluation. If your financial transition requires fast local action across the Oklahoma border, our team is standing by to provide an immediate closing solution through our dedicated home buying company in Lawton.

You don’t have to carry the financial burden of a massive property alone. Let us buy the property as-is, take on the transaction and holding risks, and put your hard-earned equity back into your bank account so you can settle your accounts and step into your next chapter with absolute peace of mind.